Map: Indian States by Solar Energy Capacity (2025)

Discover India's solar power landscape in 2025! Rajasthan leads, followed by Gujarat at. Explore state-wise rankings and key trends.

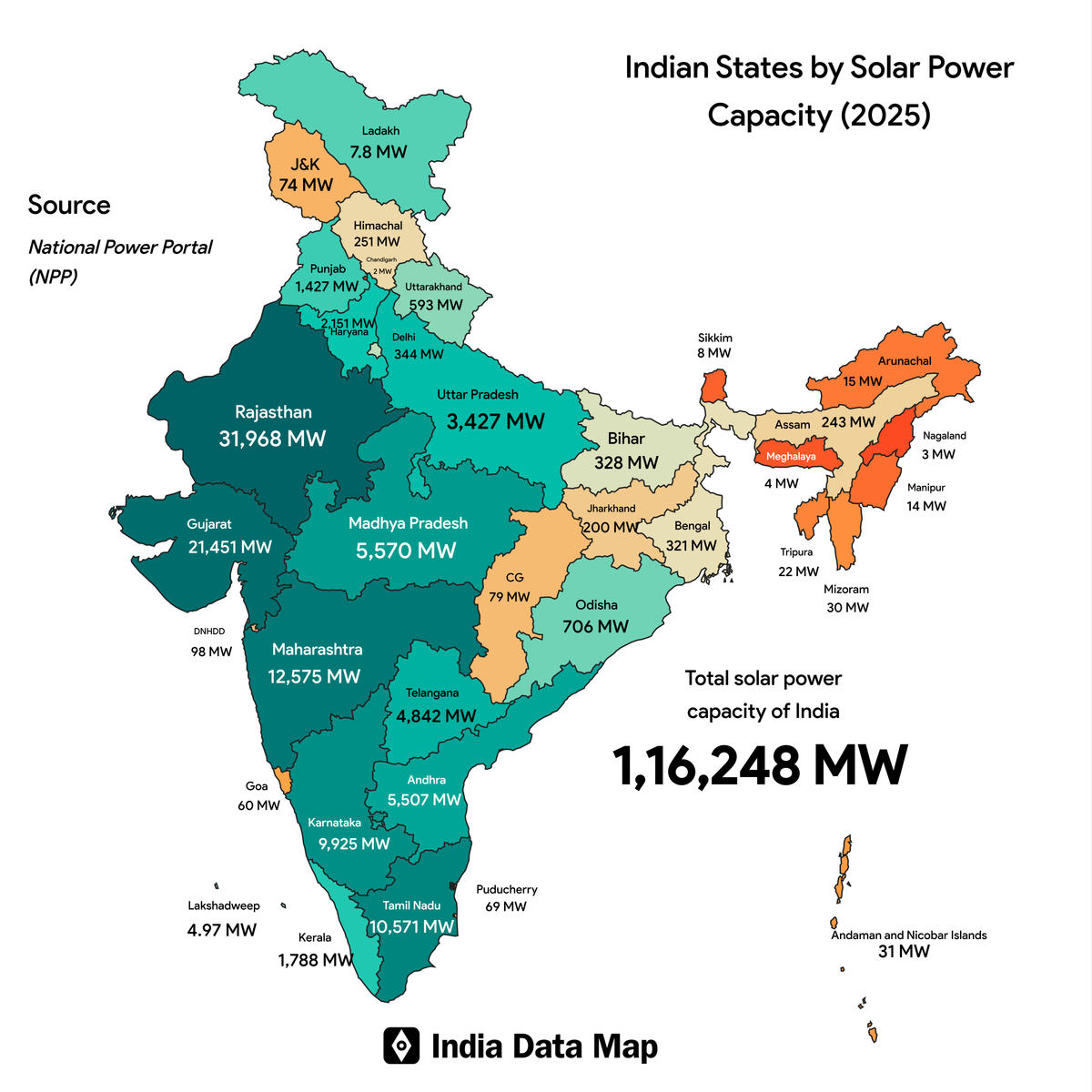

India's solar energy sector is lighting the way towards a sustainable future, boasting a national installed solar capacity of 116,247.83 MW as of May 31, 2025.

From the sun-drenched deserts of Rajasthan to the urban rooftops of Gujarat, various states and union territories throughout India are tapping into solar power on a remarkable scale.

| Rank | State/Union Territory | Solar Power Capacity (MW) |

|---|---|---|

| 1 | Rajasthan | 31968 |

| 2 | Gujarat | 21451 |

| 3 | Maharashtra | 12575 |

| 4 | Tamil Nadu | 10571 |

| 5 | Karnataka | 9925 |

| 6 | Madhya Pradesh | 5570 |

| 7 | Andhra Pradesh | 5507 |

| 8 | Telangana | 4842 |

| 9 | Uttar Pradesh | 3427 |

| 10 | Haryana | 2151 |

| 11 | Kerala | 1788 |

| 12 | Punjab | 1427 |

| 13 | Odisha | 706 |

| 14 | Uttarakhand | 593 |

| 15 | Delhi | 344 |

| 16 | West Bengal | 321 |

| 17 | Bihar | 328 |

| 18 | Jharkhand | 200 |

| 19 | Himachal Pradesh | 252 |

| 20 | Assam | 243 |

| 21 | Dadra and Nagar Haveli and Daman and Diu | 98 |

| 22 | Chandigarh | 79 |

| 23 | Jammu and Kashmir | 74 |

| 24 | Puducherry | 69 |

| 25 | Goa | 60 |

| 26 | Andaman and Nicobar Islands | 31 |

| 27 | Mizoram | 30 |

| 28 | Tripura | 22 |

| 29 | Arunachal Pradesh | 15 |

| 30 | Manipur | 14 |

| 31 | Ladakh | 8 |

| 32 | Sikkim | 8 |

| 33 | Lakshadweep | 5 |

| 34 | Meghalaya | 4 |

| 35 | Nagaland | 3 |

| 36 | Chhattisgarh | 0 |

Key Insights from the Solar Map

Rajasthan Shines Brightest: Leading the nation, Rajasthan boasts 31,967.69 MW of solar capacity, driven by mega-projects like the Bhadla Solar Park, one of the world’s largest. Its desert terrain and abundant sunlight make it a solar powerhouse.

Gujarat’s Solar Dominance: With 21,451.33 MW, Gujarat secures second place, excelling in both ground-mounted and rooftop solar, supported by progressive policies and industrial infrastructure.

Top Five Powerhouses: Maharashtra (12,575.27 MW), Tamil Nadu (10,570.88 MW), and Karnataka (9,925.44 MW) round out the top five, collectively contributing over 40% of India’s solar capacity. These states showcase a blend of industrial demand and renewable energy adoption.

Small Contributors: Smaller regions like Lakshadweep (4.97 MW), Meghalaya (4.28 MW), and Nagaland (3.17 MW) have modest capacities, reflecting their limited land and infrastructure but growing interest in solar.

Chhattisgarh’s Zero: Surprisingly, Chhattisgarh reports 0 MW of solar capacity, a stark contrast to its 25,465.72 MW total power capacity, which is dominated by thermal sources (92.29%).

Fascinating Observations

Desert Duo’s Lead: Rajasthan and Gujarat collectively represent nearly 46% of India’s solar capacity, taking advantage of their dry climates and extensive land area. The solar capacity of Rajasthan alone is three times that of Maharashtra, underscoring its unparalleled scale.

Southern Strength: The southern states, including Tamil Nadu, Karnataka, and Andhra Pradesh (5,507.48 MW), are at the forefront of solar energy, boasting high proportions of non-fossil energy sources (for instance, Karnataka: 72.01% non-fossil). Their technology-driven economies and supportive policies are propelling this expansion.

Urban vs. Rural Divide: Urban centers such as Maharashtra and Haryana (2,151.39 MW) excel in rooftop solar installations, whereas rural regions like Uttar Pradesh (3,427.49 MW) and Bihar (328.34 MW) are increasing their capacities, likely enhanced by initiatives such as the PM Suryaghar Yojana.

Northeast’s Slow Start: The northeastern states, including Nagaland, Meghalaya, and Manipur (13.79 MW), are positioned at the lower end of the spectrum, indicating limited infrastructure and lower rates of solar adoption, despite having high non-fossil energy shares (for example, Meghalaya: 100%).

Union Territories’ Modest Role: Union territories such as Dadra and Nagar Haveli and Daman and Diu (97.90 MW) and Chandigarh (78.85 MW) provide small yet significant contributions to solar capacity, frequently achieving 100% non-fossil power due to their minimal reliance on thermal energy.

Why It Matters

India’s solar landscape reflects a dynamic interplay of geography, policy, and innovation.

Rajasthan and Gujarat lead with natural advantages, while southern states like Tamil Nadu and Karnataka show how industrial and tech ecosystems fuel solar growth.

However, the low or zero capacities in states like Chhattisgarh and northeastern regions highlight the need for targeted investments to ensure equitable adoption. As India aims for 500 GW of renewable capacity by 2030, this state-wise snapshot underscores both progress and opportunities for growth.